The Federal Reserve has cut its benchmark interest rate once again, but even Fed Chair Jerome Powell warns that the move will not be a panacea for the housing market.

"The housing market faces some really significant challenges," Powell said following Wednesday's vote. "And I don't know that, you know, a 25 basis point decline in the federal funds rate is going to make much of a difference for people."

Powell noted that the housing market remains undersupplied, with many homeowners who refinanced at sub-3% rates unwilling to move and give up their lower rate.

"We're a ways away from that changing. Also we're just—we haven't built enough housing in the country for a long time," he said. "We can raise and lower interest rates, but we don't really have the tools to address, you know, a secular housing shortage, structural housing shortage."

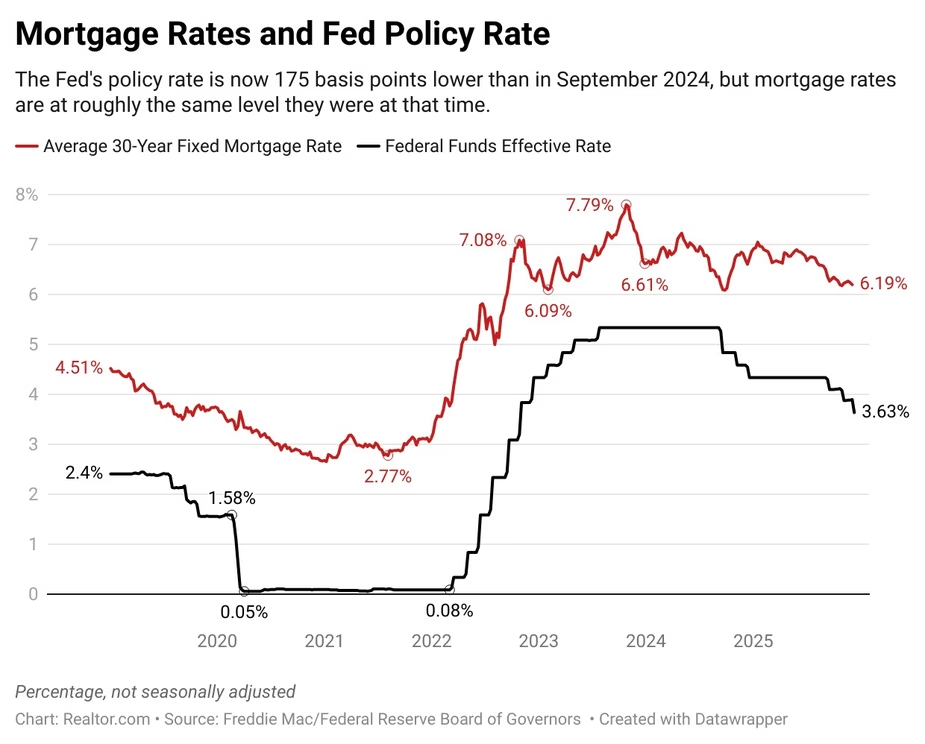

Wednesday's decision takes the Fed's benchmark overnight rate down to a range of 3.5% to 3.75%, marking the third consecutive cut since September and the lowest rate since 2022.

The Fed policy rate is now 1.75 percentage points lower than in September 2024, but mortgage rates have not experienced commensurate declines. In fact, last week's average mortgage rate of 6.19% remains slightly higher than the two-year low reached in September 2024.

That's because the Fed controls only short-term rates used for overnight lending between commercial banks, while longer-term rates such as mortgages are set by the free market, hinging on investor expectations about future inflation and monetary policy.

This week's Fed cut was already largely priced in to mortgage rates, and movement in the bond markets suggests the decision will have little immediate impact on mortgage borrowers.

Recent rate relief sparks uptick in buyer activity

Mortgage rates climbed slightly higher between the October and December Fed meetings, as markets assessed the outspoken and sometimes conflicting outlooks issued by FOMC members.

Despite the upward drift, mortgage rates have remained close to their lowest level in more than a year, potentially unlocking affordability for homebuyers on the edge of being able to purchase a home.

That's already spurred additional demand from homebuyers, which could accelerate heading into 2026, says Vishal Garg, founder and CEO of online mortgage platform Better.com.

"With mortgage rates falling to a one-year low, we’ve seen purchase activity begin to pick up," Garg tells Realtor.com®. "There are millions of Americans who’ve been sitting on the sidelines, waiting for affordability to improve, and now, with rates easing and home prices stabilizing, we’re seeing those buyers reenter the market."

Garg says he expect a noticeable uptick in purchase mortgage applications and lock volume this fall and winter, especially from first-time homebuyers and move-up buyers who now find payments more manageable.

Likewise, Alyssa Soto Brody, co-founder of real estate sales and marketing firm Powered by DMT, says that her teams in New York City and Miami have seen a "robust surge" of new contracts, calling the latest Fed rate cut "a psychological boost more than anything else."

"Buyers aren’t waiting for dramatic rate cuts, they’re acting now, and even a modest adjustment from the Fed would only accelerate the pace," she says.

Indeed, prospective homebuyers who are holding out hope for dramatic relief on mortgage rates may face disappointment.

The Realtor.com economic research team's national housing forecast for 2026 anticipates that mortgage rates will largely hover around current levels throughout next year, averaging 6.3%.

"While this may be disappointing to buyers hoping for even lower rates, mortgage rates are expected to be low enough to offset price gains, causing the monthly cost of buying a home to drop in 2026 for the first time since 2020 even as home prices rise," says Realtor.com Chief Economist Danielle Hale. "Coupled with rising incomes, affordability will improve."

Still, the future is not set in stone. Ivan Sher, a luxury real estate adviser in Las Vegas, predicts that President Donald Trump's imminent nomination of a new Fed chair could spark a rally in bond markets, driving mortgage rates lower next year.

"As rates decline, demand increases and home prices rise quickly, making today an opportunity to benefit from current pricing—wait, and the additional equity is likely to go to the seller, not you," he tells Realtor.com.

Rate cut to benefit builders and developers

Although Wednesday's rate cut isn't expected to have a major impact on mortgage rates, it could substantially benefit homebuilders and developers, who will see relief on financing costs for new projects.

"A 25-basis-point cut may sound small, but on a $40 million construction loan it adds up fast, and can save seven figures over the life of a project," says Garret Weyand, partner at California development firm Cedar Street Partners.

"It’s a clear signal that inflation is easing, lending channels can start to reopen, and if mortgage costs come down too, buyers suddenly have more purchasing power. That combination is exactly what this market needs to start moving again,” adds Weyand.

Source: Keith Griffith for Realtor.com

Comments