How Fannie Mae’s updated underwriting opens the door for more homebuyers

What changed?

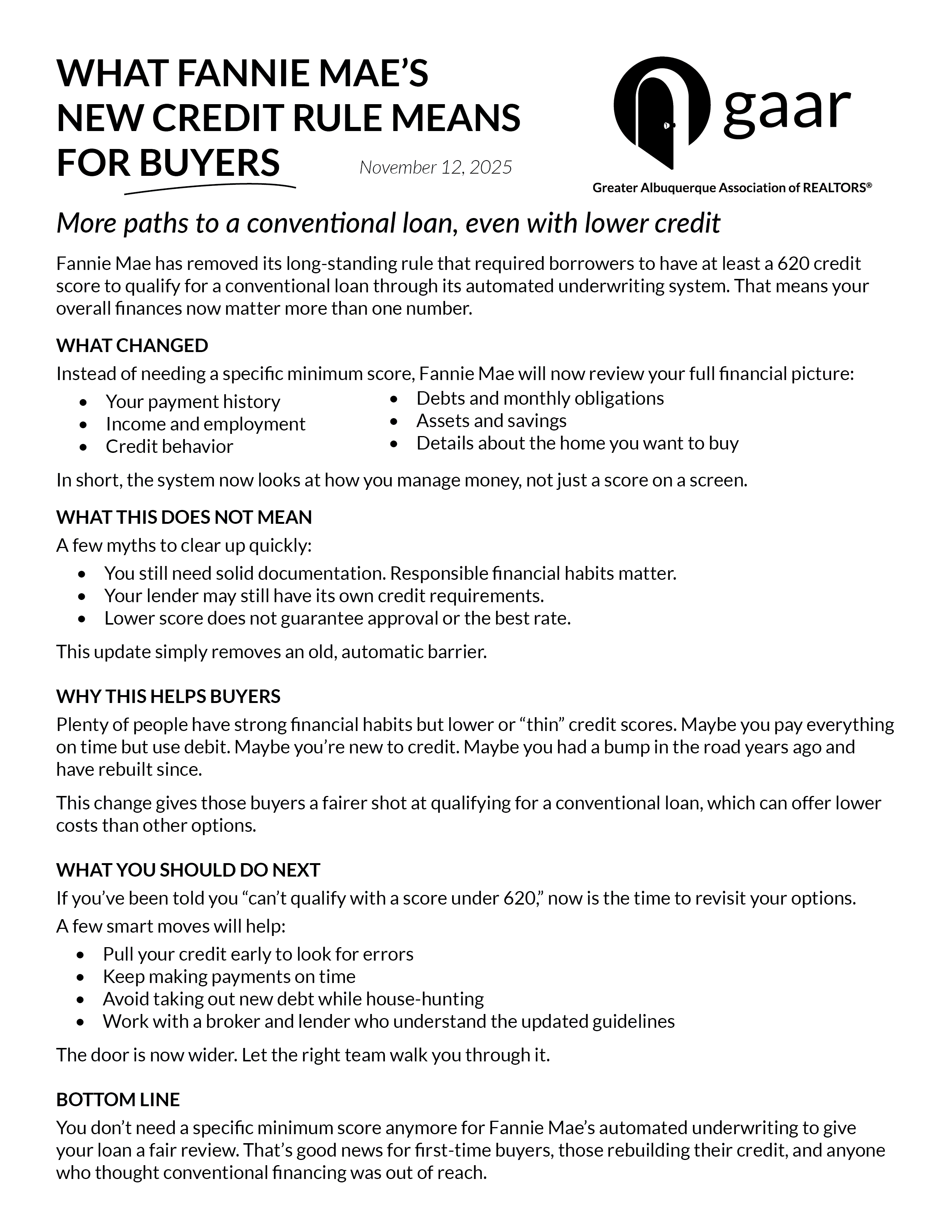

As of loans submitted on or after November 16, 2025, Fannie Mae’s automated underwriting system (Desktop Underwriter® (DU®)) will no longer require a minimum credit score of 620 for individual borrowers for conventional loans eligible for sale to Fannie.

Instead of a hard score-floor, DU will evaluate a borrower using Fannie’s proprietary risk models — weighing credit history, debt, income, assets, property characteristics, and more.

Why this matters:

- For brokers and borrowers: If a buyer’s score was under 620, they may have been automatically excluded from conventional financing. Now, there’s a chance their full profile can be reviewed.

- For the market: It signals a shift toward more inclusive underwriting practices, potentially expanding access for those with “thin” or non-traditional credit histories.

- For risk & compliance teams: One less bright-line numeric cutoff; greater emphasis on holistic evaluation and documentation.

What this doesn’t mean

Before you get too excited (and start advertising “no credit score needed!”), there are important caveats:

- Lender overlays still apply. While Fannie removed its minimum score requirement for DU eligibility, individual lenders may still enforce their own minimums, or private mortgage insurance (PMI) providers may.

- It’s not a guarantee. Removing the 620 floor doesn’t mean approval at any score. The borrower still must present sufficient income, assets, acceptable credit history (even if non-traditional), and the overall file must meet underwriting standards.

- Credit scores still matter. Although DU will no longer require a minimum score, credit scores will still be pulled and considered. In other words, this is about eligibility for DU’s approve/eligible response, not eliminating credit risk evaluation.

- Nontraditional credit rules changed. For borrowers with no traditional credit profile (i.e., no credit or installment accounts reported), DU will trigger documentation/homebuyer education requirements rather than relying solely on a numeric score.

What brokers should tell their buyers

Here are key talking points you can use in your marketing or buyer consultations:

- “If your credit score was holding you back under 620 for conventional financing, this change may open the door.”

- “We still need to look at your full financial profile — income stability, debt-to-income, assets, payment history — but the automatic ‘below-620 = no’ barrier is gone for Fannie-eligible loans.”

- “Let’s gather all your documentation and run your profile with a lender who operates banks or wholesale channels that deliver to Fannie. Even though the guideline changed, some lenders may have their own score threshold — so it’s wise to shop around.”

- “If you have thin credit or nontraditional credit (for example, mostly rent and utilities on-time payments but few installment/credit card accounts), this rule change also helps: DU will now allow for that kind of profile to get through the automated review process in some cases.”

- “Still, this is not a green light to ignore your credit. Payment history and credit behavior still matter—so keep making payments on time, managing your balances, and avoid new large debts as we prepare for loan submission.”

How does this align with current affordability pressures?

In our market — Albuquerque and New Mexico more broadly — housing affordability is under strain: elevated interest rates, rising home prices, and fewer first-time buyers. For many would-be buyers, credit score has been a barrier even when fundamentals looked solid.

By removing the 620 floor, Fannie expands conventional financing access to more people. Conventional loans often have lower mortgage insurance costs (versus FHA) and are more widely available. From a broker’s vantage, this means you'll want to reassess certain prospects who previously seemed stuck in “credit-score limbo.”

What to keep an eye on

- Performance outcomes. With lower-score or alternative-credit borrowers in the pool, watch how these loans perform. If defaults creep up, we may see new overlays or investor pressure.

- Lender behavior. Some lenders will immediately embrace the change and promote “score no longer required” messaging; others may delay or keep internal minimums. As a broker, you’ll want to know which lenders are early adopters.

- PMI provider thresholds. Even if Fannie accepts the loan, PMI may require a minimum score. That could affect cost or eligibility.

- Rate and fee impact. Because borrowers with lower scores likely represent higher risk, pricing may reflect that. Make sure buyers understand that approval doesn’t necessarily mean “best rate” without negotiation.

- Credit-education opportunity. For buyers who barely missed the old cutoff, this is a chance to revisit their profile, pull credit early, correct errors, boost assets, pay down debt, and gather nontraditional credit documentation. Your value as a broker includes guiding them through this.

Bottom line

For brokers and buyers in the field, this update from Fannie Mae is meaningful. It doesn’t rewrite the underwriting rulebook entirely, but it breaks a barrier. If you’ve been telling clients “you need a 620 score or you’re stuck in non-conventional territory,” that message is now outdated (at least for Fannie-eligible loans).

As always, the key is preparation. Work the file early, ensure income and liabilities are sound, and gather documentation. Score is no longer the automatic gate-keeper — but everything else still counts.

Buyer Handout: Share-Ready Explainer on Fannie Mae’s New Credit Rule

A simple, consumer-friendly explainer you can email, print, or use in consultations.

Click on the image below to download the PDF

Comments